Trust Administration for Businesses: Protecting Corporate Legacy

Most business owners focus on day-to-day operations and miss a critical reality: without proper trust administration for businesses, their life’s work can unravel during transitions or after death.

At Law Offices of Roshni T. Desai, we’ve seen how the right trust structure protects both your business continuity and your family’s financial security. This guide walks you through the essentials of business trust planning, common mistakes to avoid, and concrete steps to build a lasting legacy.

What Trust Administration Really Means for Your Business

Trust administration for businesses differs fundamentally from managing a personal trust because it protects ongoing operations, maintains continuity, and preserves the value of assets that generate income. When you establish a trust for your business, you create a legal structure that holds your company assets, real estate, or investment interests outside of your personal name. A trustee then manages these assets according to your written instructions, which means your business continues operating when you become incapacitated or pass away. Without this structure, your business enters probate, which can take months or years-during which time operations may stall, customers may leave, and key employees may find other work. The trustee you select carries fiduciary duties to act in the best interests of your beneficiaries while following your trust document precisely, so choosing the right trustee (whether an individual, corporate trustee, or a combination) directly affects how smoothly your business transitions.

Business Trusts Handle Complexity Personal Trusts Cannot

A business trust must account for ongoing tax filings, payroll obligations, customer contracts, and employee management in ways that personal trusts simply do not. When you hold a business inside a trust, the trustee must understand not only real estate and investment accounts but also how to maintain the business’s operational value during transitions. Personal trusts typically manage static assets like bank accounts or investment portfolios; business trusts manage dynamic operations. This means the trustee needs either knowledge of your industry or the authority to hire professionals-accountants, business managers, attorneys-to keep the company running. State law varies significantly on how trusts can hold business interests, so the trust document must comply with your state’s regulations while giving the trustee enough flexibility to respond to market changes.

Why Waiting to Plan Costs You Money and Time

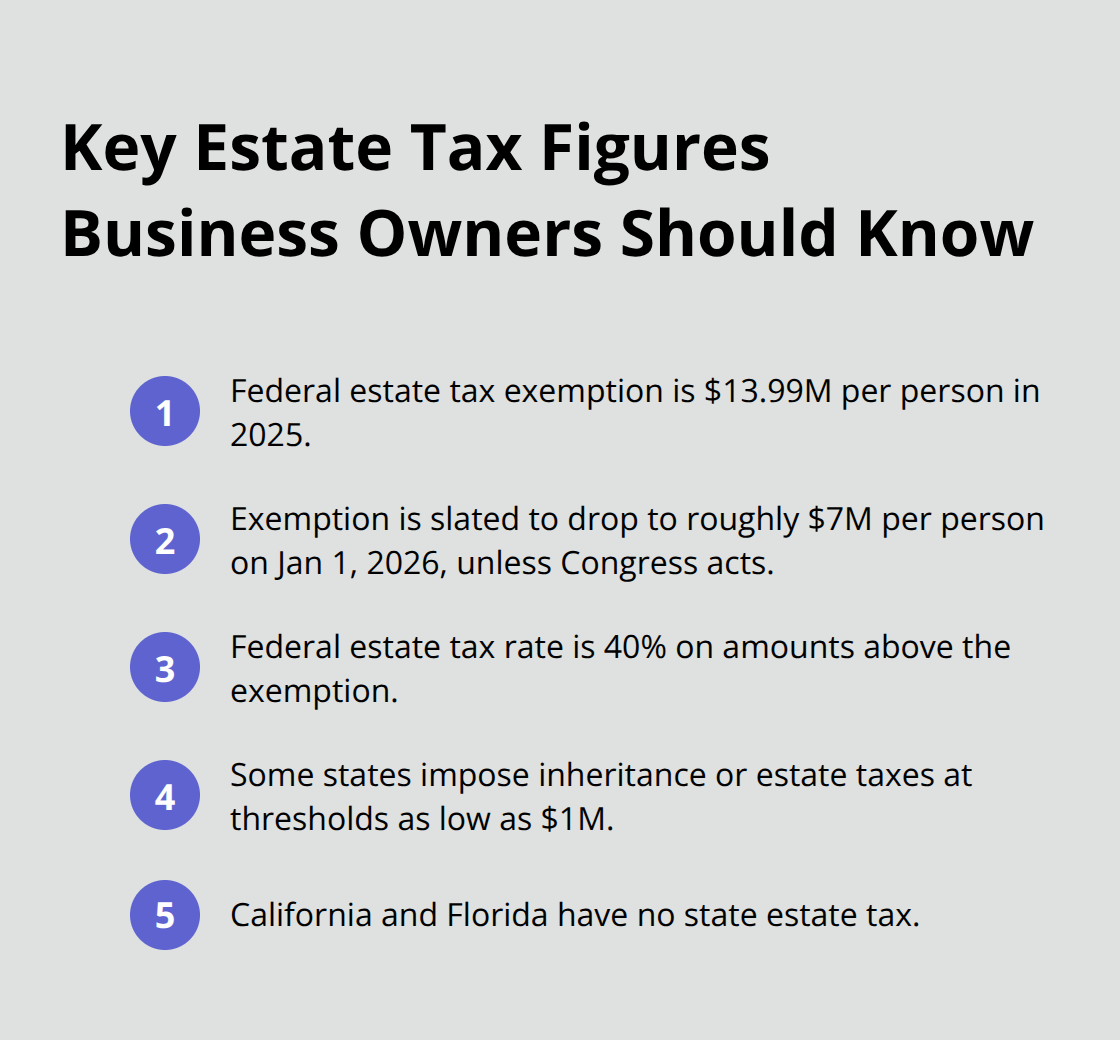

Business owners who delay trust planning often discover that their informal arrangements do not hold up during transitions. If your business is your primary asset (and for most small business owners it is), then without liquidity planning and proper trust structure, your heirs face a difficult choice: sell quickly at a discount to raise cash for estate taxes, fire-sale the business to outsiders, or struggle to maintain operations while paying estate taxes from personal funds. The federal estate tax exemption stands at $13.99 million per person in 2025, which sounds high until you realize that a successful business with real estate can easily exceed this threshold. State taxes compound the problem; California has no state estate tax, but other states impose inheritance or estate taxes at lower thresholds.

A properly structured business trust reduces or eliminates these taxes as part of an overall estate strategy and provides ongoing control over who runs the business after you’re gone.

The Real Cost of Inaction

Without proper planning, your family loses both the business and a significant portion of its value to taxes and forced sales. A trustee with clear authority to manage the business prevents the operational paralysis that occurs when courts must approve every decision. The trust document itself becomes your voice-it tells the trustee exactly how you want the business handled, who should lead it, and when distributions should occur. This level of control transfers to your beneficiaries without the delays and public scrutiny of probate. The next section explores how trusts actively protect business continuity during the critical transition periods when your business faces its greatest vulnerability.

How Trusts Keep Your Business Running When You Cannot

When a business owner becomes incapacitated or dies without a trust in place, the business enters a legal freeze. Courts must approve major decisions, customers lose confidence, and employees scatter to competitors. A properly structured trust prevents this collapse by giving your chosen trustee immediate authority to manage operations, pay bills, negotiate contracts, and maintain cash flow without waiting for probate court approval.

Immediate Authority Protects Your Business Value

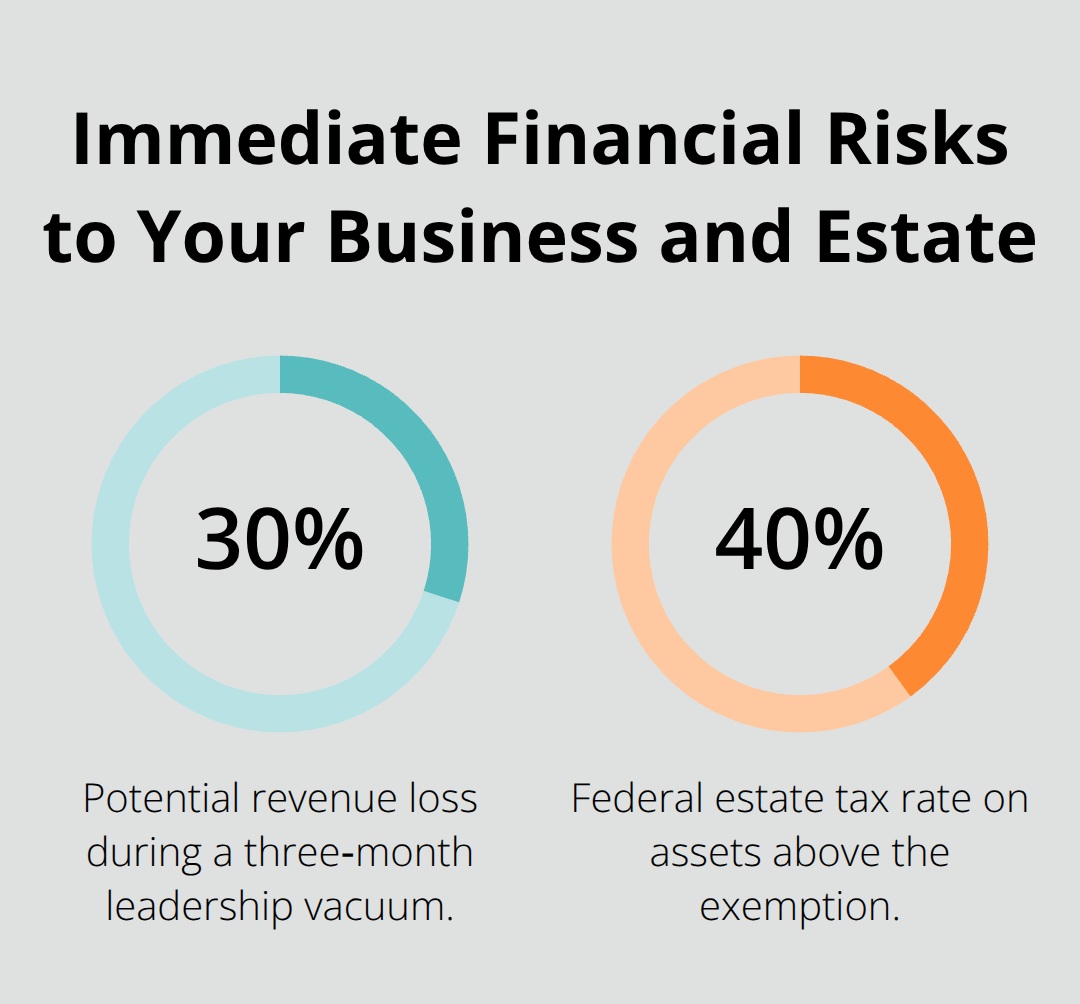

The trustee steps in seamlessly because the trust document already specifies how the business should run, who holds decision-making power, and what decisions require beneficiary input. This continuity matters enormously during the first 90 days after your incapacity or death-the window when most businesses lose their value. If your business generates $500,000 annually and loses 30% of revenue during a three-month leadership vacuum, you lose $125,000 in value that your family will never recover.

A corporate trustee or a successor trustee with business knowledge prevents this loss by keeping operations intact.

Your trustee can also hire a business manager or keep existing leadership in place if that serves the business better than direct trustee involvement. Your trust document should name specific individuals or entities who make operational decisions, set compensation for key employees, and authorize the trustee to reinvest profits or distribute them to beneficiaries. This clarity eliminates paralysis and protects the asset that matters most to your family’s financial security.

Strategic Trust Structures Reduce Your Tax Burden

The federal estate tax exemption of $13.99 million per person in 2025 disappears on January 1, 2026, when it drops to roughly $7 million per person unless Congress acts. A successful business worth $10 million then faces potential federal estate taxes of 40% on assets above the exemption, costing your heirs $1.2 million or more. A Credit Shelter Trust (also called an AB Trust or Bypass Trust) preserves both spouses’ exemptions and prevents the unused exemption from one spouse from vanishing when the first spouse dies. Married couples without this structure waste hundreds of thousands in tax savings.

If you own real estate alongside your business, a Grantor Retained Annuity Trust lets you transfer appreciating property to beneficiaries at a discounted value for gift tax purposes while you retain income from the asset during your lifetime. The discount depends on IRS interest rates and the length of your retained interest, but it can reduce the taxable value of a property by 30% to 50%. A Life Insurance Trust owned separately from your personal estate removes life insurance proceeds from your taxable estate entirely, providing tax-free money to pay estate taxes or fund a buy-sell agreement that keeps the business in family hands.

State taxes amplify these concerns; Florida has no state estate tax, but other states impose inheritance or estate taxes at thresholds as low as $1 million. The right trust structure for your specific situation requires understanding your state’s rules, your business valuation, and your family’s goals.

Control Stays With Your Vision, Not the Courts

A trust gives you final say over who runs the business, when beneficiaries receive distributions, and what happens if circumstances change. Without a trust, a probate court decides these matters based on state law, not your wishes. If you want your business to pass to your daughter but she lacks management experience, your trust can direct the trustee to hire a professional manager or keep existing leadership in place until she completes business education. You can also include incentive provisions that reward beneficiaries for education, business performance, or staying involved in the company.

If family conflict exists, you can appoint an independent corporate trustee rather than a family member, eliminating disputes over decisions. The trust document itself becomes your voice across decades-it tells future trustees and beneficiaries exactly how you want your legacy managed. This level of control protects both the business and family relationships by removing personal conflicts from operational decisions. Your trustee follows your written instructions, not family politics or courtroom arguments. The next section addresses the operational and legal pitfalls that derail many business owners who fail to update their trust documents as their companies grow and market conditions shift.

Common Pitfalls in Business Trust Administration

Most business owners create a trust once and never touch it again. This mistake costs thousands in unnecessary taxes and leaves your trustee scrambling to manage a business that no longer matches the trust document you signed five years ago. Your business structure changes-you acquire a second location, bring in a partner, pivot your service offering, or restructure ownership to reduce liability. Meanwhile, your trust sits frozen with outdated instructions about how the old business should run. When transitions happen, the trustee either ignores parts of your trust document (creating legal exposure) or follows outdated terms that no longer serve your business or family.

Outdated Trust Documents Paralyze Your Trustee

A trust that worked perfectly for a sole proprietorship becomes a liability when you incorporate or form an LLC. State law governs how different entity types can be held in trust, and your original trust document may not give the trustee adequate authority to manage an S-corporation, hold membership interests in an LLC, or navigate the tax complications of pass-through entities. Your trustee needs explicit authority in writing to handle the specific assets your business now owns, the operational decisions that matter today, and the tax implications of your current structure. Without this clarity, your trustee either makes decisions that violate the trust terms or delays action while seeking legal guidance-both outcomes that harm your business during critical moments. We recommend reviewing your trust every two to three years, or immediately after any major business change: a merger, significant acquisition, new partner, or shift to a different business structure.

Key Person Departures Create Immediate Crises

Many business owners assume their trust automatically solves succession when a critical employee or partner dies or leaves. It does not. A key person leaving creates an immediate operational crisis-clients call looking for their relationship contact, vendors question continuity, and employees wonder if the business will survive. Your trust document must explicitly address what happens when a key manager, partner, or you become unavailable. This means identifying specific individuals or roles essential to operations, clarifying whether the trustee has authority to hire replacements, and funding mechanisms like key person insurance that provides cash to keep the business running or buy out a departing partner’s stake.

If your business depends on your technical skills, your sales relationships, or a specific partner’s contributions, life insurance owned inside a Life Insurance Trust removes proceeds from your taxable estate while providing immediate liquidity to bridge the leadership gap. The insurance proceeds go directly to your trust, giving the trustee cash to hire interim management, retain key staff through bonuses, or execute a buy-sell agreement that keeps the business in family hands rather than forcing a fire-sale to outsiders. Without this insurance funding, your trust has authority but no money-and a trustee cannot pay salaries or maintain operations from thin air. Your trust document should also specify whether the trustee should continue operating the business, sell it, or wind it down, because different situations call for different responses.

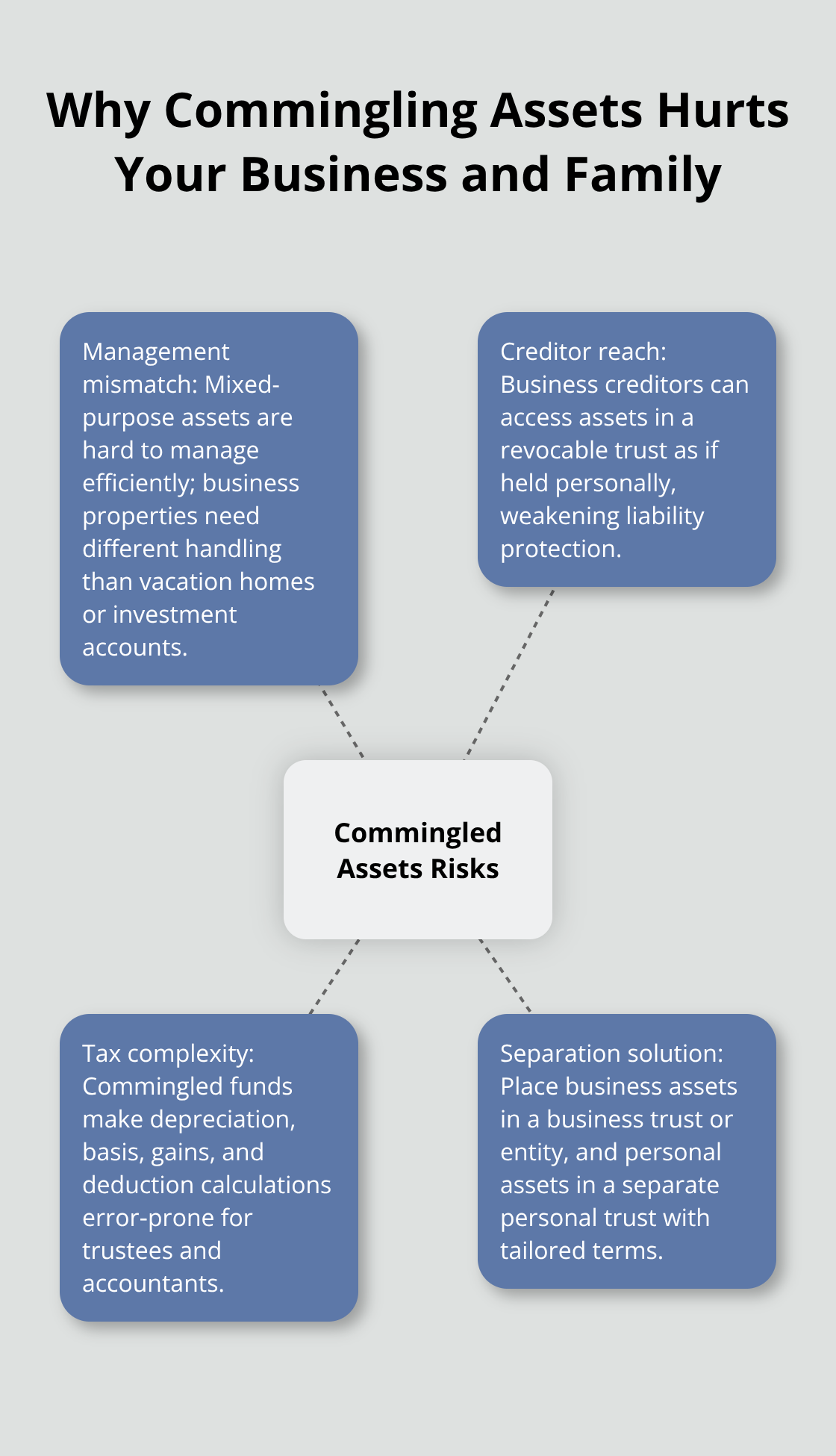

Commingled Assets Destroy Liability Protection

Business owners frequently hold business assets, personal real estate, investment accounts, and family heirlooms in a single revocable trust without separating them. This approach creates three serious problems. First, your trustee cannot efficiently manage assets with completely different purposes-a business property generating operational income requires different handling than a vacation home held for family enjoyment or an investment account funding retirement.

Second, creditors of your business can reach business assets held in a revocable trust the same way they reach assets in your personal name, eliminating the liability protection that a separate business entity should provide. If your business faces a lawsuit and loses, a judgment creditor can attach business assets held in your personal trust, potentially compromising both the business and family assets.

Third, tax treatment diverges sharply between business and personal assets, and commingling funds makes it nearly impossible for your trustee and accountant to calculate depreciation, cost basis, capital gains, and deduction eligibility correctly. A properly structured plan separates business assets into a business trust or holds them in a business entity (corporation or LLC) whose interests are then held in your family trust. Personal real estate, investment accounts, and heirlooms go into a separate personal trust with different management terms. This separation allows your trustee to manage each category according to its specific needs-operational decisions for business assets, investment strategy for securities, and distribution decisions for personal property based on family wishes rather than business requirements. It also preserves liability protection because creditors of your business cannot reach personal assets held separately, and creditors of your personal estate cannot reach business assets.

Final Thoughts

Trust administration for businesses protects what you’ve built and ensures your family inherits a functioning operation, not a legal mess. The pitfalls we’ve covered-outdated documents, unplanned key person transitions, and commingled assets-derail most business owners who treat trust planning as a one-time event rather than an ongoing process. Your business changes constantly, and your trust must change with it.

Start by reviewing your current trust document if one exists and ask yourself whether it reflects your business today, whether your trustee has clear authority to manage your specific assets, and whether your family knows who will lead the company when you cannot. If you lack a trust entirely, the cost of inaction far exceeds the cost of planning (a business worth $2 million can lose 30 percent of its value during a three-month leadership vacuum, and estate taxes can consume another 40 percent without proper structuring). That leaves your family with less than half of what you built.

We at Law Offices of Roshni T. Desai help business owners across Southern California build trusts that protect both operations and family assets. Schedule a free consultation to discuss how trust administration can secure your business legacy for the next generation.