Elder Law Trust Attorney: Planning for Care and Legacy

Most seniors put off planning until a health crisis forces their hand. By then, critical decisions fall to family members or the courts instead of you. An elder law trust attorney helps you take control now-protecting your assets, your family, and your wishes for the future. We at Law Offices of Roshni T. Desai guide clients through this process with clarity and care.

What Elder Law Really Includes

Elder law stretches far beyond wills and trusts. It covers healthcare directives, powers of attorney, Medicaid planning, long-term care strategies, and asset protection from nursing home costs. According to the National Academy of Elder Law Attorneys (NAELA), a comprehensive elder law plan typically includes durable powers of attorney, healthcare directives, and trust-based strategies for legacy protection.

Why Wills Alone Fall Short

Many seniors think a will alone handles everything, but wills only direct what happens after death. They say nothing about who makes medical decisions if you become incapacitated tomorrow, or how to pay for assisted living in five years. Incapacity planning matters far more than most people realize. Healthcare decisions, financial management during your lifetime, and long-term care funding are the real priorities. Without these pieces in place, your family faces court intervention, delayed medical care, and unnecessary costs.

The Five-Year Rule That Changes Everything

Medicaid planning deserves special attention because it requires specific timing and structure. Assets placed in an irrevocable trust must sit there for at least five years before long-term care is needed to protect Medicaid eligibility. Start that process too late and you’ll lose benefits when you need them most. The five-year look-back rule is not flexible, and small mistakes in trust design can jeopardize everything.

Why Waiting Costs More Than Planning

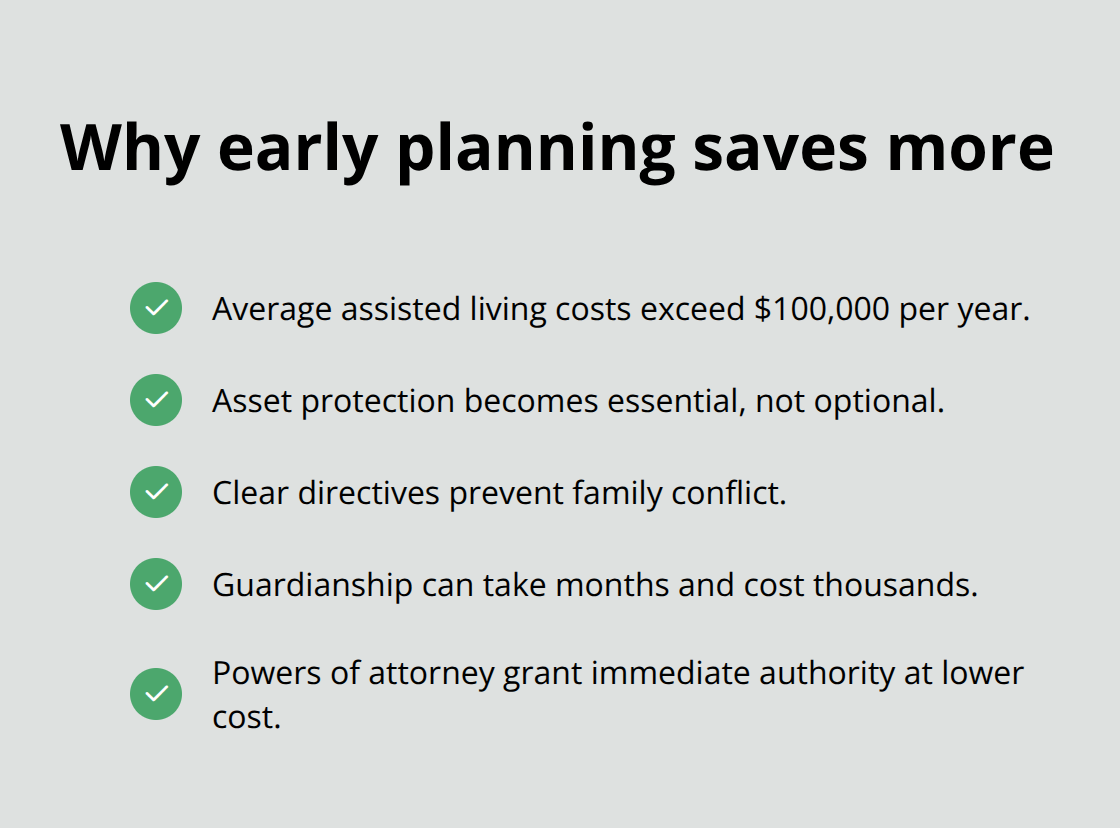

Planning now gives you control over what happens next. Early planning also protects your assets more effectively because you have time to structure trusts, fund them properly, and let the five-year Medicaid look-back period run its course before care becomes necessary. Seniors who plan ahead avoid probate, reduce estate taxes, and keep family assets intact. Those who wait often watch their life savings drain to nursing home costs that could have been protected with proper Medicaid planning.

The cost of long-term care in the United States averages over $100,000 annually for assisted living facilities and significantly more for skilled nursing, making asset protection strategies essential rather than optional. Planning also prevents family conflict because your wishes are documented and clear, not left for relatives to guess about or fight over. When incapacity happens without a healthcare directive in place, Florida courts may require guardianship proceedings that cost thousands of dollars and take months to complete. A durable power of attorney and healthcare proxy cost far less and give your chosen agent immediate authority.

Common Errors That Drain Family Resources

Seniors commonly fail to name beneficiaries on retirement accounts and life insurance, leaving those assets to pass through probate or to ex-spouses instead of intended heirs. They also neglect to update beneficiary designations after divorce, remarriage, or the birth of grandchildren, creating unintended consequences. Another frequent error is holding property jointly without understanding the tax and liability consequences (joint ownership triggers probate in some states, exposes assets to creditors of either owner, and can disqualify Medicaid eligibility if nursing home care becomes necessary).

Many also create trusts but fail to fund them properly, leaving assets in their personal name and defeating the entire purpose of the trust structure. Using online services or templates for complex situations like blended families, special needs dependents, or significant assets leaves gaps that create costly litigation later. The cost of fixing mistakes after someone passes or becomes incapacitated far exceeds the cost of planning correctly upfront.

These errors reveal why the next step-creating a comprehensive care and legacy plan-requires careful attention to detail and proper coordination of all your documents.

Building Your Care and Legacy Plan Today

Your healthcare decisions and financial management during your lifetime matter far more than what happens after you’re gone, yet most seniors focus only on the latter. A comprehensive care and legacy plan requires three coordinated layers: durable powers of attorney that name someone to act on your behalf immediately if needed, trusts that protect assets and bypass probate delays, and long-term care strategies that preserve your savings from nursing home costs. These pieces must work together, not exist as separate documents gathering dust in a drawer.

Powers of Attorney: Immediate Protection Against Incapacity

Start with durable powers of attorney because incapacity can strike at any moment and without them, your family faces expensive guardianship court proceedings. A durable financial power of attorney lets your chosen agent pay bills, manage investments, and handle property sales without court involvement the moment you sign it, even if you’re still healthy and capable. A healthcare power of attorney designates someone to make medical decisions aligned with your values if you cannot communicate, preventing doctors from turning to courts or family conflicts to determine treatment.

These documents cost far less than guardianship proceedings, which average $3,000 to $5,000 in court costs alone and take months to complete in Florida. The power of attorney takes effect immediately upon signing, giving your agent authority today rather than forcing your family to petition a judge later.

Trusts: Structuring Assets for Your Specific Goals

Next, structure your assets through trusts that serve your specific goals. Revocable living trusts let you manage your property during life while avoiding probate after death, keeping your affairs private and reducing settlement delays that can stretch six months to over a year in probate court. Irrevocable trusts, in contrast, remove assets from your ownership entirely, shielding them from creditors and potentially qualifying you for Medicaid benefits if nursing home care becomes necessary.

The five-year Medicaid look-back period means assets must sit in an irrevocable trust for at least 60 months before long-term care is needed to protect eligibility. Funding these trusts correctly is non-negotiable; assets left in your personal name defeat the entire structure. Many seniors create trusts but fail to retitle property deeds, transfer investment accounts, and update beneficiary designations on retirement accounts and insurance policies, leaving those assets outside the trust where they intended them to be.

Long-Term Care Planning: Coordinating Strategy with Timing

Long-term care planning requires coordinating your trust strategy with Medicaid timing because the average cost of assisted living in the United States exceeds $100,000 annually and skilled nursing care runs significantly higher. Asset protection through irrevocable trusts works only if you plan ahead; waiting until a health crisis forces immediate nursing home placement leaves no time for the five-year look-back period to run its course.

Your healthcare directive should address not just life-or-death decisions but also your preferences for living arrangements, rehabilitation versus comfort care, and your wishes regarding feeding tubes or extraordinary measures. An elder law attorney coordinates these documents so your power of attorney aligns with your trust structure, your healthcare preferences connect to your long-term care funding strategy, and every asset is positioned according to your actual goals rather than left to chance.

The next step involves understanding how trusts and asset protection strategies shield your property from creditors, taxes, and the costs that threaten to drain your family’s resources.

How Trusts Protect Your Assets from Creditors, Taxes, and Long-Term Care Costs

Shielding Property from Creditors and Nursing Home Claims

Trusts stop creditors and the government from seizing your property in ways wills simply cannot. When you own property in your personal name, creditors can sue you, win a judgment, and place a lien against your home or bank accounts. When you own that same property inside an irrevocable trust, the creditor has no claim because you no longer own it legally-the trust does. This distinction matters enormously in elder law planning because nursing homes, medical providers, and Medicaid recovery programs pursue personal assets aggressively. An irrevocable trust removes assets from your personal estate before a crisis hits, placing them beyond reach of these claims. The five-year Medicaid look-back rule requires assets to sit in the trust for at least 60 months before nursing home care becomes necessary, but once that period passes, those assets are protected.

Avoiding Probate and Reducing Settlement Costs

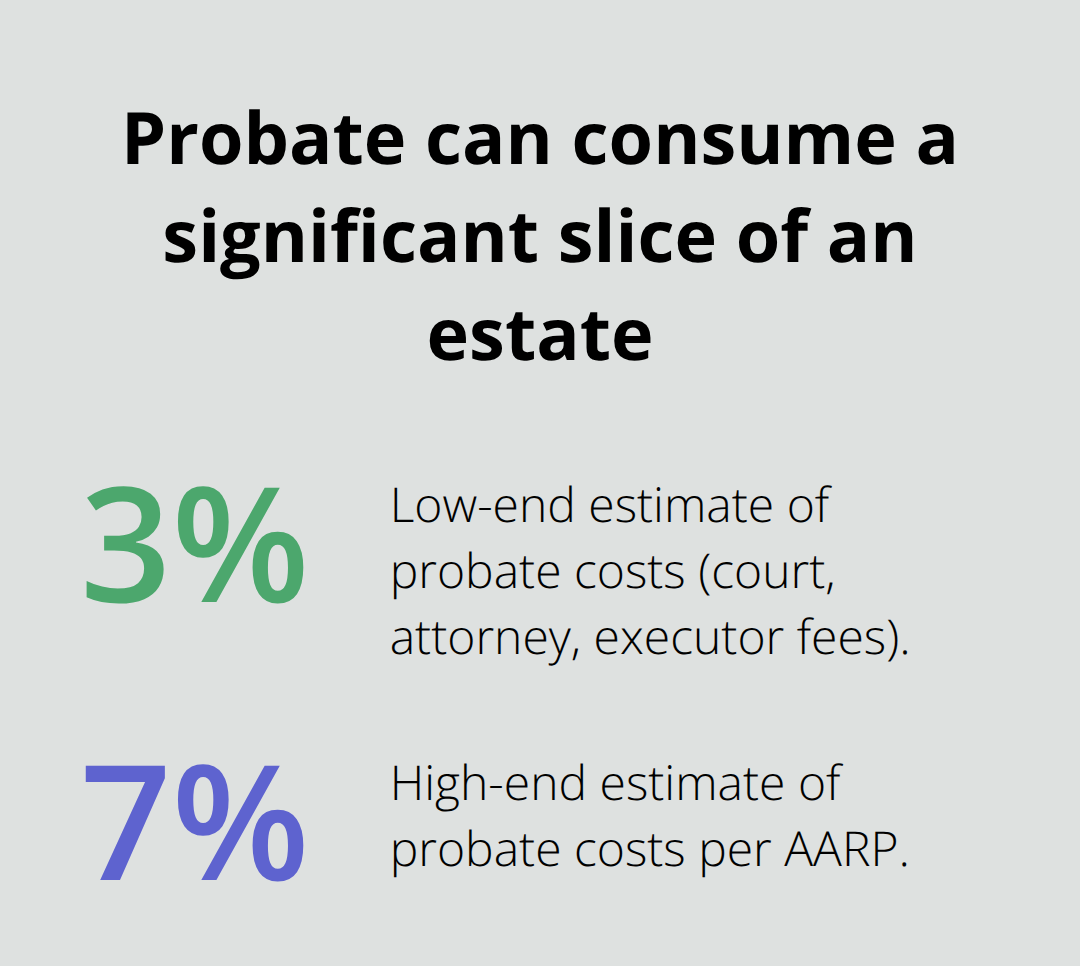

Revocable living trusts offer different benefits: they avoid probate entirely, keeping your estate settlement private and reducing delays that typically stretch six months to over a year in court. Probate also costs money-court fees, attorney fees, and executor compensation can consume 3% to 7% of your estate’s value according to the American Association of Retired Persons. A revocable trust bypasses these costs entirely because assets transfer directly to beneficiaries outside the probate process.

Minimizing Estate and Income Taxes Through Trust Structure

Taxes present another serious threat that trusts can minimize. Federal estate taxes apply to estates exceeding $13.61 million in 2024, but state-level taxes hit much lower thresholds, and proper trust structuring reduces what your heirs owe. Irrevocable trusts remove assets from your taxable estate, meaning their growth after funding is never subject to federal estate tax. A married couple can use spousal lifetime access trusts or qualified personal residence trusts to transfer significant wealth to children while minimizing gift and estate taxes. These strategies require careful drafting because mistakes cannot be undone once an irrevocable trust is signed.

Coordinating Incapacity Planning with Trust Authority

Healthcare decisions and incapacity planning demand coordination with your trust structure because incapacity can arrive without warning and leave your family unable to access accounts or make medical decisions. A durable healthcare power of attorney must name someone to make medical decisions aligned with your actual values-not just life-or-death choices but also preferences for rehabilitation versus comfort care, feeding tubes, and living arrangements. Your financial power of attorney should grant your agent immediate authority to manage bank accounts, pay bills, and handle investments the moment you sign it, even if you remain healthy and capable today. This prevents your family from needing guardianship court proceedings that cost $3,000 to $5,000 and take months to obtain in Florida. Your HIPAA authorization must specifically grant your agent access to medical records and conversations with doctors, otherwise providers can refuse to share information even with your spouse. Coordinate these documents with your trust so your trustee and your financial power of attorney agent communicate regularly and understand your wishes. If they conflict-your trustee wants to preserve assets while your power of attorney agent needs to spend money on care-confusion and family tension result.

Protecting Blended Families, Special Needs Beneficiaries, and Non-Traditional Relationships

Blended families and complex situations demand trust structures that protect each spouse’s children without creating conflict or unintended consequences. Many seniors in second marriages hold property jointly with their current spouse, assuming it passes to that spouse at death and then to their own children afterward. That assumption is wrong. Joint property passes entirely to the surviving spouse, who then controls whether your children ever receive anything. A qualified terminable interest property trust, or QTIP trust, solves this problem by providing income to your spouse for life while guaranteeing the principal eventually passes to your designated heirs. Special needs beneficiaries require special needs trusts that preserve their eligibility for government benefits like Medicaid and Supplemental Security Income. Assets in a properly drafted special needs trust do not count toward the $2,000 resource limit that disqualifies beneficiaries from these programs. Without a special needs trust, an inheritance can destroy eligibility and leave your disabled child without essential benefits. Unmarried partners need explicit documentation because state law offers no automatic rights to partners who are not married. A trust names your partner as beneficiary and grants authority through powers of attorney; without these documents, your partner has no claim to your assets or decision-making authority if you become incapacitated. Adult children with substance abuse issues or poor financial judgment can receive distributions through a spendthrift trust that restricts their access and prevents creditors from seizing their inheritance. These situations require specific language and careful planning because generic templates cannot address the nuances of blended families, special needs, or non-traditional relationships.

Final Thoughts

Planning for care and legacy protects your family from financial devastation and ensures your wishes guide decisions when you cannot make them yourself. The documents you create today-powers of attorney, trusts, healthcare directives, and long-term care strategies-prevent costly court proceedings, preserve assets from nursing home costs, and eliminate confusion about your medical preferences. Without these pieces in place, your family faces guardianship expenses, probate delays, and decisions made by courts instead of people who know you.

An elder law trust attorney coordinates these elements so they work together toward your actual goals rather than existing as separate documents. The five-year Medicaid look-back period, trust funding requirements, beneficiary designation updates, and incapacity planning all demand attention to timing and detail. Small mistakes in trust design or asset titling can jeopardize Medicaid eligibility or leave assets outside your trust where creditors can reach them.

Your next step is scheduling a consultation with an elder law professional who understands both estate planning and long-term care strategies. We at Law Offices of Roshni T. Desai provide personalized estate planning and probate services across Southern California, covering wills, living and irrevocable trusts, powers of attorney, and elder law planning with over 25 years of experience. Contact us today for a free consultation with flexible home or office visits that fit your schedule.