Trust Real Estate Administration: Efficient Management of Property in Trust

Managing real property held in trust requires a different approach than handling your own home or investment property. Trustees face unique legal obligations, tax considerations, and administrative responsibilities that demand careful attention.

We at Law Offices of Roshni T. Desai help trustees navigate trust real estate administration with clarity and confidence. This guide walks you through the essential steps to manage, maintain, and potentially sell trust properties effectively.

What Trust Real Estate Administration Really Means

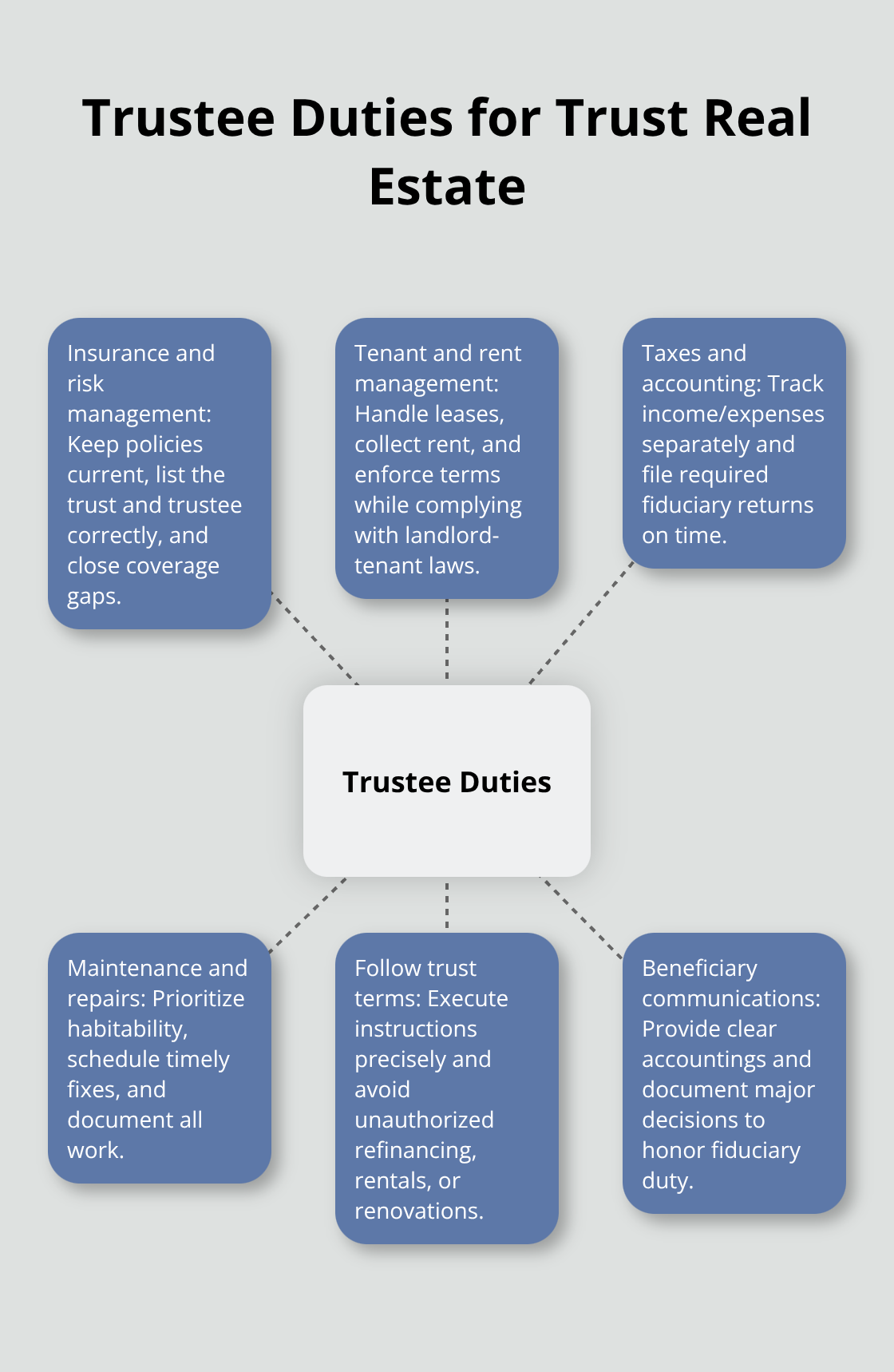

Trust real estate administration is the process of managing, maintaining, and potentially selling property owned by a trust after the grantor dies or becomes incapacitated. This goes far beyond simply holding a deed in a trust’s name. As a trustee, you become responsible for every aspect of the property-from ensuring insurance stays current to handling tenant relations, collecting rent, paying property taxes, and making repairs. The trustee acts as a fiduciary, meaning you are legally bound to act in the beneficiaries’ best interests, not your own. This fiduciary duty is enforced by law, and breaches can result in personal liability. Unlike owning property personally, where you make decisions based on your preferences, trust property administration requires you to follow the trust document’s instructions precisely.

If the trust specifies how the property should be managed or when it should be sold, those terms control your actions. You cannot simply decide to refinance, renovate extensively, or rent the property to a family member at below-market rates without clear authorization from the trust terms.

Why Trust Property Demands a Different Approach

Managing property in a trust differs fundamentally from personal ownership because the property belongs to the trust, not to you individually. This distinction creates legal separation-the trust is a separate entity with its own tax identification number and obligations. When you own a rental property personally, you can deduct losses against your income and make strategic decisions about timing repairs or sales. Trust property operates under different tax rules. Income generated from trust real estate is taxable to the trust itself, and capital gains are calculated based on a stepped-up basis at the grantor’s death, which can significantly reduce tax liability if property is sold shortly after. However, if the property appreciates substantially after entering the trust, that appreciation is taxable when sold. You must file a fiduciary income tax return for the trust if it generates income above certain thresholds, adding administrative complexity. Additionally, beneficiaries have legal rights to information about the property and how you manage it. You must provide accounting statements and justify significant decisions. This transparency requirement protects beneficiaries but means you cannot operate with the privacy you would have managing personal property.

The Real Obstacles Trustees Encounter

Trustees managing real estate face obstacles that personal property owners rarely encounter. First is the challenge of securing and protecting the property immediately after the grantor’s death. If the home sits empty or tenants vacate, pipes freeze, roofs leak, and security becomes a concern. Securing adequate insurance that names the trustee and trust properly takes time, and gaps in coverage expose you to liability. Second is the complexity of managing tenancies. If the property generates rental income, you inherit the landlord’s obligations-maintenance requests, lease enforcement, and potential eviction proceedings. Many trustees lack experience with tenant law and make mistakes that expose them to liability or lost income. Third is the tax and accounting burden. Unlike personal property, trust real estate requires separate accounting, potentially separate tax returns, and coordination with the trust’s overall tax strategy. Missing deadlines for property tax payments or failing to adjust insurance as property values change can trigger penalties. Fourth is the decision about whether to keep or sell the property. Beneficiaries often hold different opinions-some want to preserve the family home, others want liquidity. You must balance these competing interests while following the trust’s terms and acting in everyone’s best interests. If the trust grants discretion about selling, the decision becomes yours, and any beneficiary unhappy with that choice may challenge you.

Moving Forward with Clarity

Understanding these foundational responsibilities prepares you for the practical steps ahead. The next section walks you through assessing what property the trust actually owns, inventorying its condition and value, and establishing the systems you need to manage it effectively.

Managing Trust Real Estate from Day One

Locate and Inventory Every Property

Start by obtaining certified copies of the trust document and identify every property the trust owns. Many trustees discover assets titled in ways they didn’t expect-a vacation home in another state, a commercial building held jointly, or raw land acquired years ago. Pull property tax records, deed information, and any mortgage or lien documents. Create a physical folder or digital spreadsheet listing each property’s address, current market value, outstanding debts, annual tax amount, and insurance details. This inventory prevents costly oversights and establishes a clear picture of what you manage.

Secure Properties and Protect Against Liability

Secure the property immediately after the grantor’s death or incapacity. If the home is occupied by tenants, verify lease terms and rental payment arrangements. If vacant, inspect for damage, change locks, and photograph conditions inside and out. Contact the insurance company within days to confirm the policy names the trust and trustee correctly. Gaps in coverage expose you to personal liability if damage occurs. Homeowner’s insurance typically costs between 0.5% and 1.5% of property value annually, but trust properties sometimes require higher premiums if they’re vacant or have tenants. Shop around-you may find savings by bundling multiple properties or working with insurers familiar with fiduciary accounts.

Open a dedicated trust bank account separate from personal accounts. Deposit rental income here and pay all property-related expenses from this account. Commingling trust and personal funds is one of the fastest ways to expose yourself to liability claims and makes accounting a nightmare during beneficiary disputes.

Handle Tenant Relations and Lease Obligations

Managing tenancies demands attention to state landlord-tenant law, which varies significantly by location. If tenants occupy the property, you inherit all landlord obligations-maintenance, habitability standards, security deposit handling, and lease enforcement. Many states require landlords to maintain properties in safe, livable condition under implied warranty of habitability statutes. Failing to repair a broken furnace or address mold can result in tenant claims for reduced rent or lease termination. Document all maintenance requests in writing and respond promptly with timelines for repairs. Keep receipts and photographs.

Rental income should be tracked separately for each property and deposited into the trust account. The trust itself pays income tax on this revenue, so coordinate with a CPA familiar with fiduciary returns. If the property generates substantial rental income, the trust may need its own Employer Identification Number and separate tax return filings.

Manage Maintenance and Consider Professional Help

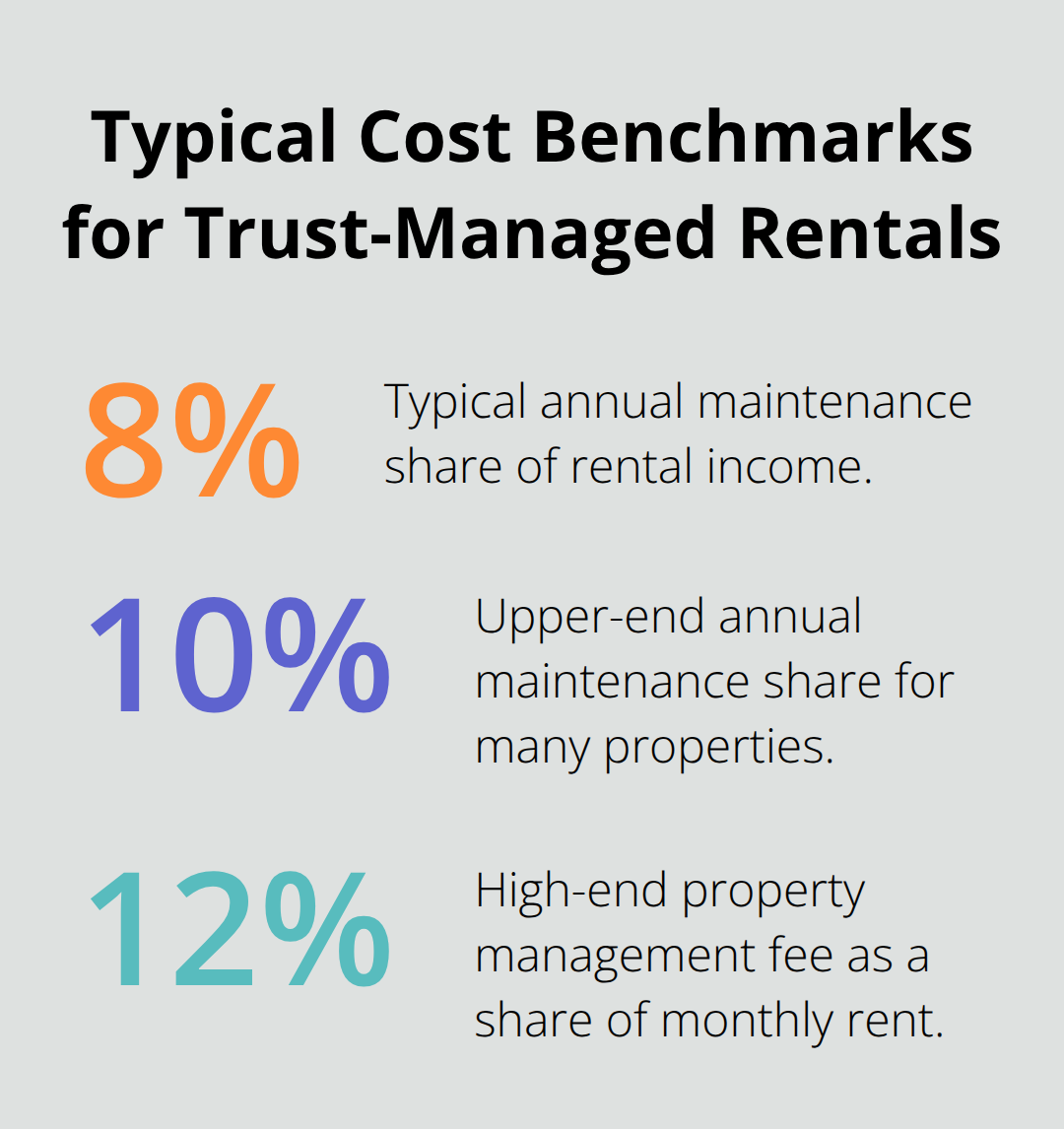

Property maintenance costs typically run 8% to 10% of annual rental income according to property management industry standards, though older buildings cost significantly more. If you lack experience managing tenants or handling maintenance coordination, hiring a property manager costs 8% to 12% of monthly rent but prevents costly legal mistakes.

The manager handles lease disputes, maintenance scheduling, and tenant screening, protecting you from personal liability.

Getting property management quotes early makes sense, especially if you’re managing multiple properties or properties in different states. Managing real estate remotely creates serious compliance risks that a professional can mitigate. With the property secured, insured, and systems in place, you’re ready to address the longer-term question of whether the trust should hold the property indefinitely or sell it to benefit the beneficiaries.

Should You Sell Trust Property or Keep It

Deciding When to Sell Trust Property

Selling trust property requires careful planning, clear documentation, and awareness of tax consequences that differ dramatically from personal home sales. Many trustees rush this decision without understanding the financial and legal implications, leading to missed tax savings or beneficiary disputes. The straightforward truth: you should sell trust property only when it aligns with the trust’s terms and genuinely benefits the beneficiaries.

If the trust grants you discretion about sales, document your reasoning in writing before listing the property. Courts and beneficiaries expect to see objective justification for major decisions. Common reasons to sell include high carrying costs that drain the estate, beneficiary requests for liquidity, inability to manage the property remotely or across multiple states, or appreciation that makes holding the asset tax-inefficient.

Evaluating Financial Performance

If a rental property generates 4% annual income but costs 8% to 10% annually in maintenance and management fees, selling makes financial sense. Properties in declining neighborhoods or those requiring major repairs drain resources faster than they generate value. Conversely, properties with stable tenants, positive cash flow, and low vacancy rates may justify holding them to benefit beneficiaries over time.

The decision hinges on the specific property, the trust’s instructions, and what actually serves the beneficiaries’ interests rather than your personal preferences. Run the numbers carefully before committing to either path.

Legal Requirements for Trust Property Sales

Selling trust real estate involves legal requirements that differ from personal home sales, primarily because you sell on behalf of the trust rather than in your own name. The deed must transfer from the trust to the buyer, and title companies will require proof of your authority as trustee. A certification of trust simplifies this process without exposing the full trust document to the title company.

Before listing, verify that the property title is clean by obtaining a title search and addressing any liens, easements, or claims against the property. If the grantor died with outstanding mortgages or property tax liens, these must be paid from trust assets before distributing proceeds to beneficiaries.

Understanding Capital Gains Tax on Trust Sales

Capital gains tax on trust property sales differs significantly from personal home sales because the stepped-up basis rule applies at the grantor’s death. If the grantor owned a home worth $400,000 at death and it sells for $450,000 six months later, the trust owes capital gains tax only on the $50,000 appreciation, not the full $450,000. This stepped-up basis represents one of the most valuable tax advantages in estate planning.

However, if the property appreciates substantially after the grantor’s death, that post-death appreciation is fully taxable. Selling quickly after death captures the stepped-up basis benefit. If a property sits in the trust for five years while appreciating $100,000, the trust pays capital gains tax on that entire $100,000. The federal long-term capital gains rate ranges from 0% to 20% depending on the trust’s income level, and most states impose additional capital gains taxes. California, for example, taxes capital gains as ordinary income with rates up to 13.3% for high-income trusts.

Coordinating Sales for Maximum Tax Efficiency

Coordinate the sale timing with a CPA familiar with fiduciary tax returns to save thousands in unnecessary taxes. If the trust owns multiple properties, selling lower-appreciation properties first preserves the stepped-up basis advantage for properties with significant appreciation. This strategic sequencing protects more of the estate’s value for beneficiaries.

Ms. Desai’s dual licensure as an attorney and real estate professional means she coordinates estate-related property sales to reduce costs, delays, and communication complications. This integrated approach prevents common mistakes where legal and tax considerations conflict.

Final Thoughts

Trust real estate administration demands attention to detail, clear documentation, and strategic decision-making at every step. You must treat trust property as a separate asset with its own legal obligations, tax implications, and fiduciary responsibilities. Secure the property immediately, maintain accurate records, manage tenants professionally, and make decisions about holding or selling based on what genuinely benefits the beneficiaries rather than personal preference.

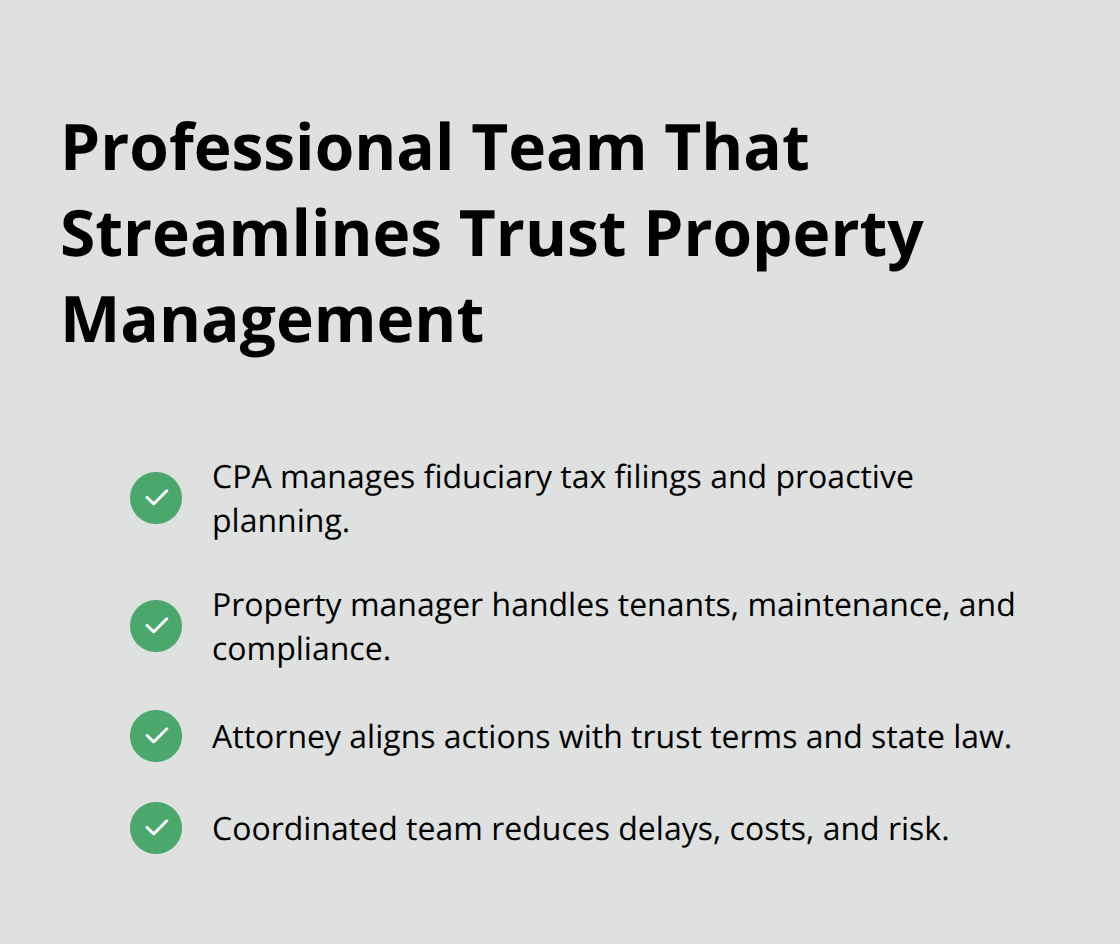

Professional support streamlines this process significantly. Managing trust real estate across multiple states, coordinating tax strategies with property sales, and navigating landlord-tenant law requires knowledge that most trustees lack. A CPA familiar with fiduciary returns prevents costly tax errors, while a property manager handles tenant relations and maintenance coordination, protecting you from legal exposure. An attorney ensures your decisions comply with the trust terms and state law, and when these professionals work together, the administrative burden drops dramatically.

If you’re managing trust property or facing decisions about whether to hold or sell, contact Law Offices of Roshni T. Desai for a free consultation. We offer flexible home or office visits to discuss your specific situation and outline a clear path forward.