Estate Administration Guidance: Practical Steps for Executors and Heirs

Losing a loved one is difficult enough without the added stress of managing their estate. At Law Offices of Roshni T. Desai, we know that executors and heirs often feel overwhelmed by the legal and financial responsibilities ahead.

This guide walks you through each phase of estate administration, from securing documents to distributing assets to beneficiaries. You’ll find concrete steps and practical advice to help you navigate the process with confidence.

What Executors Need to Know Right After Someone Passes Away

Losing a loved one is difficult enough without the added stress of managing their estate. The immediate period after someone passes away demands swift action, yet many executors waste precious time searching for documents or unsure where to begin.

Locate and Secure the Will and Estate Documents

Your first priority is locating the original will and assembling all related estate documents in one secure place. Start by checking the decedent’s home office, safe deposit boxes, and attorney files. If you cannot locate an original will, contact the person’s attorney, financial advisor, or bank directly-they often retain copies.

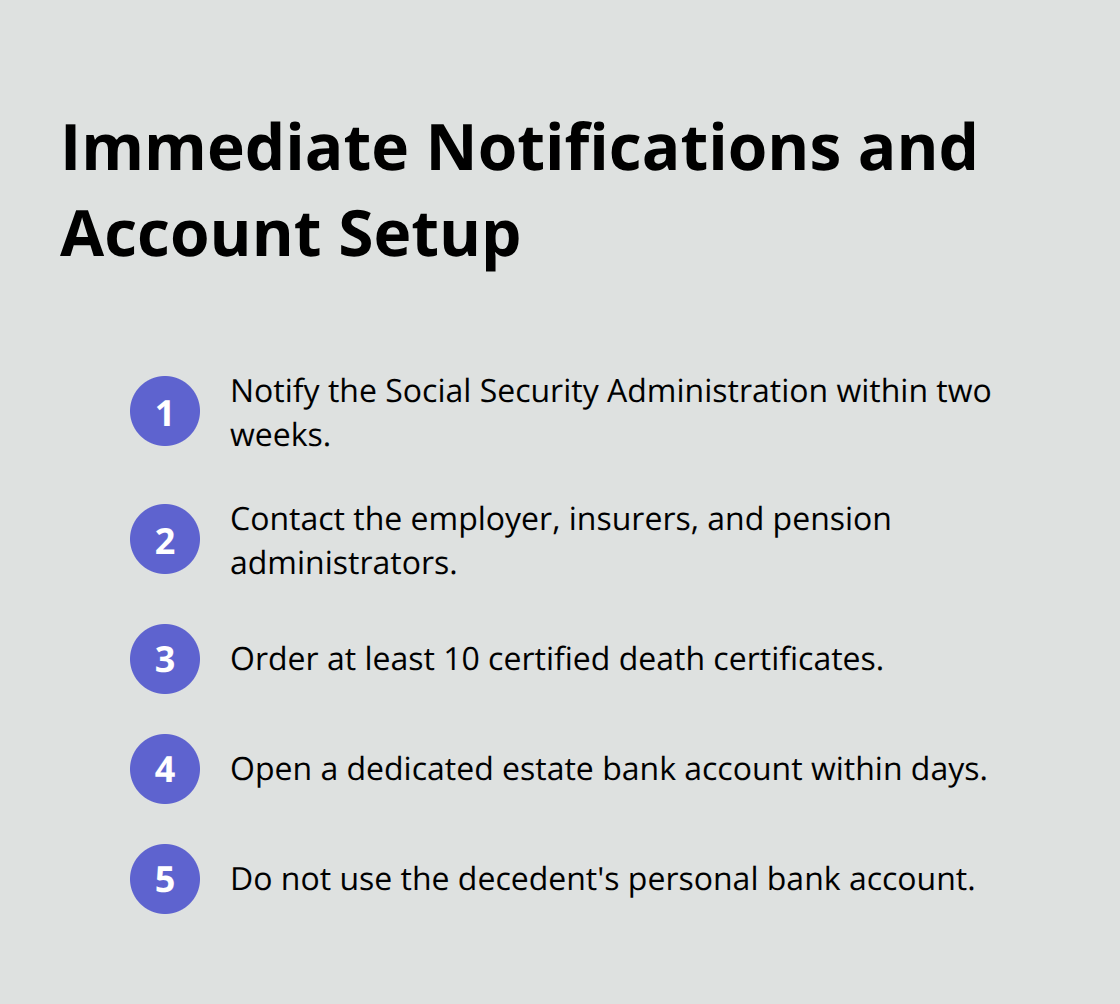

Obtain at least 10 certified copies of the death certificate from the county recorder’s office immediately. Banks, insurers, creditors, and government agencies will each demand one. This single step prevents delays that can stretch weeks.

Notify Key Institutions and Agencies

Notify the Social Security Administration within two weeks of death to stop any benefit payments and avoid overpayment issues. Contact the decedent’s employer, insurance companies, and pension plan administrators simultaneously. These entities process notifications slowly, and delays compound problems downstream.

Open a dedicated estate bank account within days of death using the proper title format-for example, Jane Smith, Executor, Estate of John Smith. This account separates estate funds from your personal finances and provides a clear audit trail that beneficiaries and courts can review. Do not deposit funds into the decedent’s personal account, as this complicates probate and raises legal questions about asset control.

Inventory Everything Immediately

Locate and document all property the decedent owned. This includes real estate, vehicles, bank accounts, investment accounts, retirement accounts, life insurance policies, business interests, jewelry, and collectibles. Create a spreadsheet listing each asset, its approximate value, and the account or title information. Some states require a formal personal property inventory filed with the probate court, so check your local requirements.

For high-value items like real estate or business interests, hire a professional appraiser within the first month. Appraisals establish the asset’s value as of the date of death, which affects both estate taxes and capital gains taxes for beneficiaries. Request that appraisers provide written documentation you can file with tax returns.

Address Creditors and Ongoing Expenses

Identify and notify all known creditors by sending formal notice within 60 days of the death. California law requires notice to creditors in probate proceedings, and failure to comply can extend creditor claim periods. Pay utility bills, mortgage payments, and property taxes on time to avoid penalties that drain estate funds.

These immediate actions establish control, prevent asset deterioration, and demonstrate fiduciary responsibility that protects you from liability. With documents secured, institutions notified, and assets inventoried, you now turn to the financial obligations that demand attention-filing tax returns and settling outstanding debts.

Managing Debts, Taxes, and Financial Obligations

File the Decedent’s Final Income Tax Return

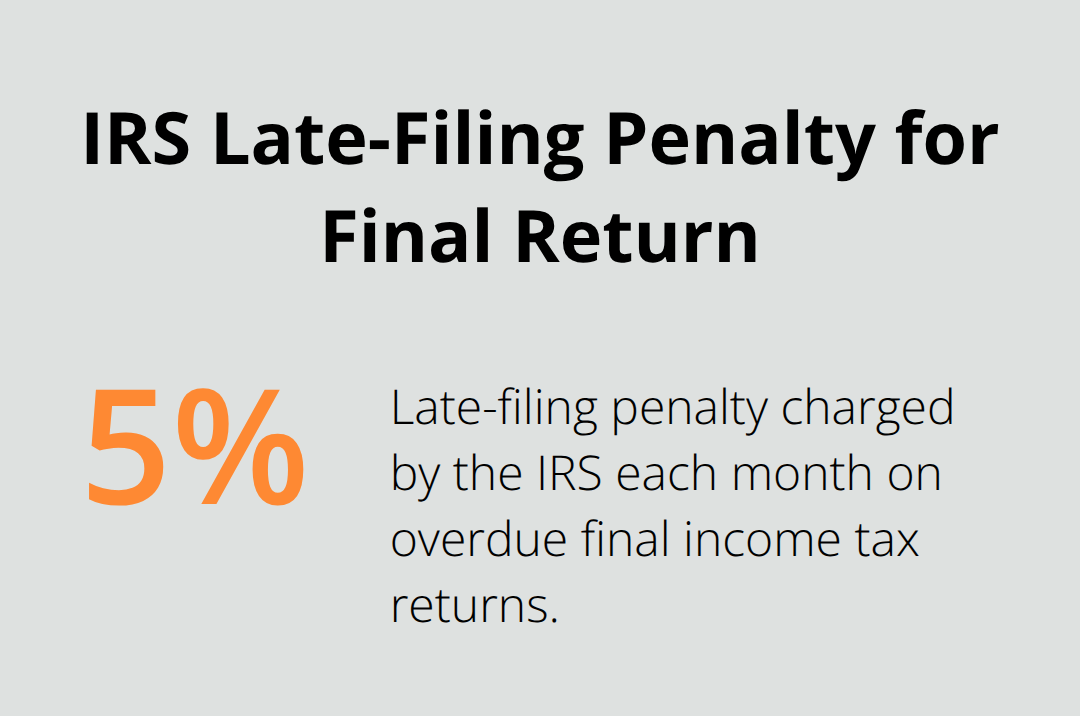

Filing the decedent’s final income tax return is non-negotiable and must happen within the standard deadline, typically April 15 following the year of death. The IRS imposes penalties of 5% per month for late filing, and interest accrues daily on unpaid taxes. Obtain an Employer Identification Number for the estate immediately from the IRS-never use the decedent’s Social Security number for estate transactions.

If the decedent earned significant income before death or the estate generates income during administration, you must file Form 1041, the fiduciary income tax return, and issue Schedule K-1s to all beneficiaries. The federal estate tax exemption rose to $15 million per individual in 2026, meaning most estates avoid federal estate taxes entirely. California has no state estate tax, so your focus shifts to income taxes and potential gift tax complications if the decedent made large gifts in prior years.

Determine Estate Tax Filing Requirements

File the federal estate tax return only if the gross estate exceeds the exemption amount or if portability rules apply-this preserves unused exemption for a surviving spouse. These returns are due nine months after death, and the deadline is absolute; extensions require formal IRS approval and typically cost time you cannot recover later.

Address Debts and Creditors Systematically

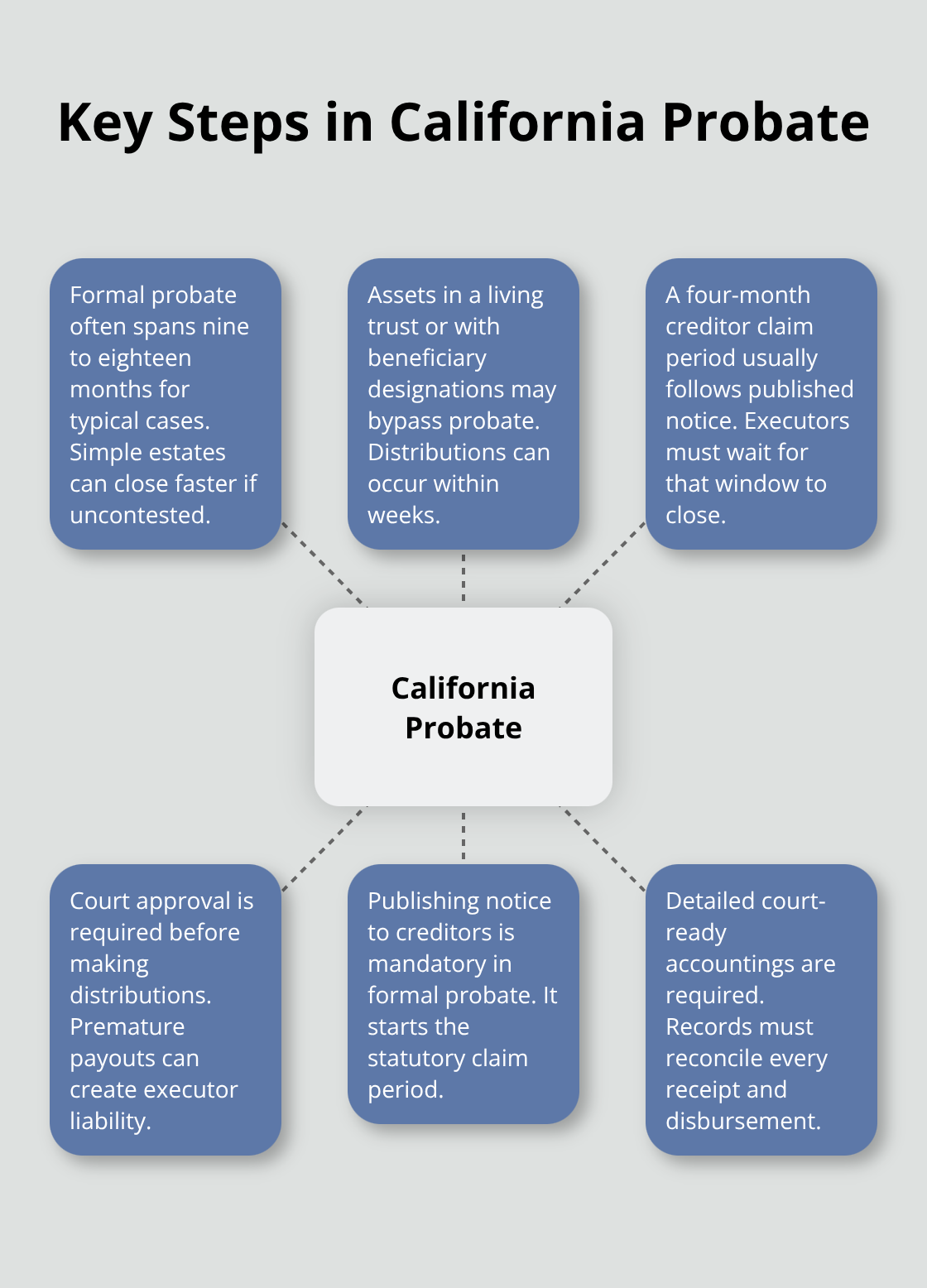

Debts and creditors demand immediate attention because unpaid obligations drain estate assets and create personal liability for you as executor. Pay utility bills, property taxes, and mortgage payments on schedule to avoid penalties that compound monthly. California law requires you to publish notice to creditors in a local newspaper, which typically opens a four-month claim period during which creditors must submit formal demands.

Prioritize secured debts like mortgages and car loans because lenders can foreclose or repossess if payments lapse. Unsecured debts like credit cards rank lower and often settle for less than the full balance if the estate lacks sufficient funds.

Obtain Professional Appraisals for Major Assets

Hire a professional appraiser for real estate and business interests within the first 60 days-appraisals establish the asset’s fair market value as of the death date, which determines capital gains taxes for beneficiaries and estate tax liability. Request written appraisals on letterhead that you can attach to tax returns. Do not guess at values or use online estimates; the IRS challenges low appraisals aggressively, and undervalued assets create unexpected tax bills years later.

Once you have clear valuations, you know exactly how much the estate owes and can plan distributions confidently. This financial clarity prevents disputes with beneficiaries who otherwise suspect mismanagement or hidden costs. With taxes filed and debts settled, you now prepare the detailed accounting records that beneficiaries require before you transfer property titles and distribute remaining assets.

Distributing Assets to Heirs and Beneficiaries

Understand California Probate Timelines

California probate takes nine to eighteen months on average, though simple estates close in six months if no disputes arise. The timeline depends entirely on whether the estate requires formal probate or qualifies for simplified procedures. If all assets passed through a living trust or via beneficiary designations on retirement accounts and life insurance, you skip probate entirely and distribute assets within weeks.

If the decedent left property titled in their name alone, formal probate becomes mandatory, and the court controls the schedule. The personal representative must publish notice to creditors, wait the full four-month claim period, file detailed accounting documents with the court, and obtain judicial approval before distributing a single dollar.

Rushing this process creates liability. Courts reject distributions made before debts and taxes are fully settled, and beneficiaries can sue you personally if they later discover unpaid creditor claims.

Maintain Detailed Accounting Records Throughout Administration

Create a detailed ledger from day one showing opening balances, all receipts and disbursements, dates, descriptions, and running balances. Include copies of appraisals, tax returns, creditor payment receipts, and professional fees paid. When probate concludes, prepare a formal accounting statement showing where every asset went and what each beneficiary received.

California courts require this accounting in formal probate cases, and beneficiaries can challenge it if numbers don’t reconcile. Beneficiaries also receive Schedule K-1 forms from the estate’s fiduciary tax return, detailing their share of estate income and deductions. Incomplete accounting invites disputes and extends the administration period by months.

Transfer Titles and Ownership After Court Approval

Title transfers must occur only after the court approves your final accounting or after the probate waiting periods expire. For real estate, obtain a certified copy of the court order or deed of distribution, then file it with the county recorder to transfer title into the beneficiary’s name. For bank and investment accounts, work directly with financial institutions using certified death certificates and court documents as proof of your authority.

Retirement accounts and life insurance proceeds pass directly to named beneficiaries and bypass probate entirely-contact those institutions immediately to process claims. For vehicles and property held in trust, transfer title by providing the trustee certification and updated deed to the Department of Motor Vehicles or relevant agency.

Obtain Receipts and Close the Estate

Obtain written receipts from each beneficiary acknowledging receipt of their distribution; these receipts protect you from later claims that distributions never occurred or were incorrect. This final step documents that you fulfilled your fiduciary duties and completed the administration process properly.

Final Thoughts

Estate administration demands careful attention to deadlines, documentation, and fiduciary responsibilities that extend far beyond the initial shock of loss. The most common mistakes executors make stem from incomplete record-keeping, missed tax deadlines, and premature asset distributions before debts are fully settled. These errors are preventable with systematic planning and professional guidance from the start.

The complexity of estate administration guidance varies dramatically depending on whether the estate includes a living trust, business interests, real property in multiple states, or significant tax exposure. What works for a simple estate with a trust may fail entirely for a larger probate case requiring court involvement. Many executors attempt to handle everything alone, only to discover months later that they missed critical filing requirements or failed to follow state-specific probate procedures.

If you feel uncertain about any step in this process, contact an attorney immediately rather than proceeding alone. The cost of professional guidance pales against the cost of correcting mistakes after they occur. We at Law Offices of Roshni T. Desai offer personalized estate planning and probate services across Southern California, including trust and probate administration tailored to your specific situation.