Irrevocable Trust Administration Guide: Managing Complex Trusts

Irrevocable trusts are powerful estate planning tools, but they come with strict rules and ongoing obligations. Once you establish an irrevocable trust, you cannot change or revoke it, which makes proper administration critical from day one.

At Law Offices of Roshni T. Desai, we help clients navigate the complexities of irrevocable trust administration. This guide covers what you need to know about managing these trusts effectively.

Understanding Irrevocable Trusts and Their Purpose

What Makes a Trust Irrevocable

An irrevocable trust becomes permanent the moment you sign and fund it. Unlike revocable trusts, which you can modify or dissolve during your lifetime, an irrevocable trust locks in its terms immediately. This permanence is not a flaw-it’s the entire point. The IRS recognizes irrevocable trusts as separate legal entities, which triggers significant tax and asset protection benefits that revocable trusts simply cannot deliver. Once assets transfer into an irrevocable trust, they no longer belong to you personally, meaning creditors cannot reach them and the IRS cannot include them in your taxable estate. You lose control, but you gain protection. This permanence also means you must structure the trust correctly before funding. Mistakes become expensive to fix, which is why working with an attorney before establishing the trust matters far more than most people realize.

Key Differences Between Revocable and Irrevocable Trusts

Revocable trusts are popular because they offer flexibility, but they fail to accomplish what irrevocable trusts do. A revocable trust avoids probate and provides privacy, but it does nothing to reduce estate taxes or shield assets from creditors. Federal estate tax applies to revocable trusts at full value when you die-currently affecting estates over $13.61 million in 2024, though this threshold drops to $7 million in 2026 unless Congress acts. Irrevocable trusts remove assets from your taxable estate entirely, potentially saving your heirs hundreds of thousands in taxes. If asset protection is your goal, revocable trusts offer zero protection because you retain control, making assets vulnerable to lawsuits and creditor claims. Irrevocable trusts create a genuine barrier. If you need income control for a spendthrift beneficiary or want to protect assets for a child with special needs, only an irrevocable structure provides the legal authority to restrict distributions. Your actual objectives determine which structure fits, not what sounds simpler.

Common Reasons to Establish an Irrevocable Trust

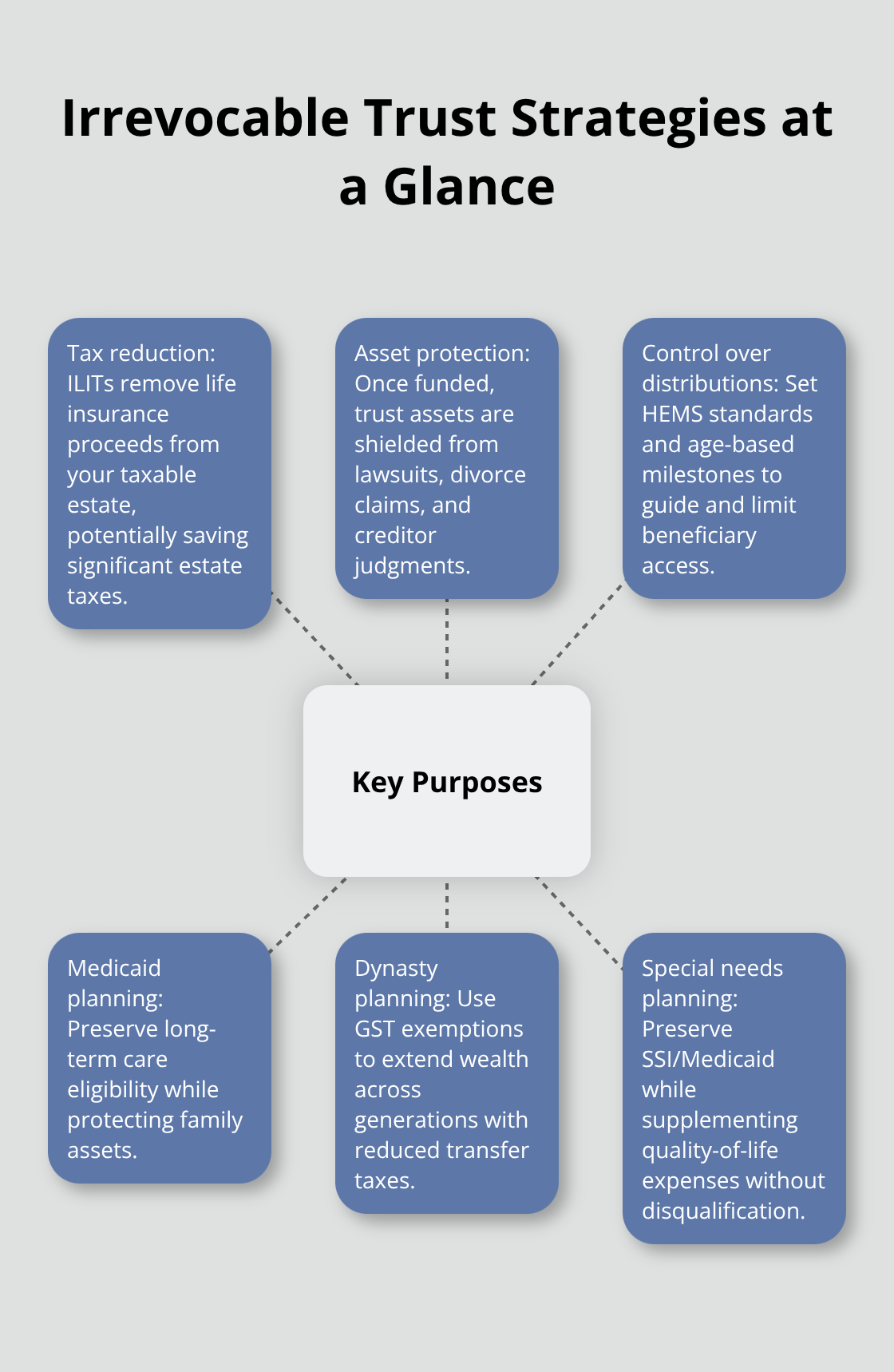

Families establish irrevocable trusts for three concrete reasons: tax reduction, asset protection, and control over distributions. Irrevocable life insurance trusts, or ILITs, remove life insurance proceeds from your taxable estate, which can save millions. If you own a $5 million life insurance policy, that death benefit counts as part of your estate and triggers estate tax liability-unless the policy sits inside an ILIT, where it passes tax-free to beneficiaries. Dynasty trusts extend wealth across multiple generations while applying generation-skipping transfer tax exemptions, allowing families to build lasting wealth without repeated estate taxes at each generational level. Medicaid planning often requires irrevocable trusts to protect assets while preserving eligibility for long-term care coverage. High-net-worth individuals use irrevocable trusts to shelter assets from business liability, divorce claims, or creditor judgments. Special needs trusts must be irrevocable to preserve government benefits for disabled beneficiaries without disqualifying them from SSI or Medicaid. Each of these strategies requires permanence-you cannot achieve them with a revocable trust.

The specific financial or family situation you face should drive the decision to establish an irrevocable trust, not general estate planning trends. Once you understand why irrevocable trusts serve your goals, the next step involves learning what a trustee actually does and how to handle the ongoing obligations that come with administration.

Managing Trustee Responsibilities and Fiduciary Duties

The Core Obligations That Define a Trustee’s Role

A trustee’s job is not theoretical-it is a series of concrete, time-sensitive obligations that directly affect whether beneficiaries receive what the trust promises and whether the trustee avoids personal liability. The moment an irrevocable trust becomes active, the trustee must obtain the original trust document, identify all beneficiaries (including potential future descendants), and inventory every asset the trust holds. This inventory step matters because missing or mislabeled assets create problems that multiply over time.

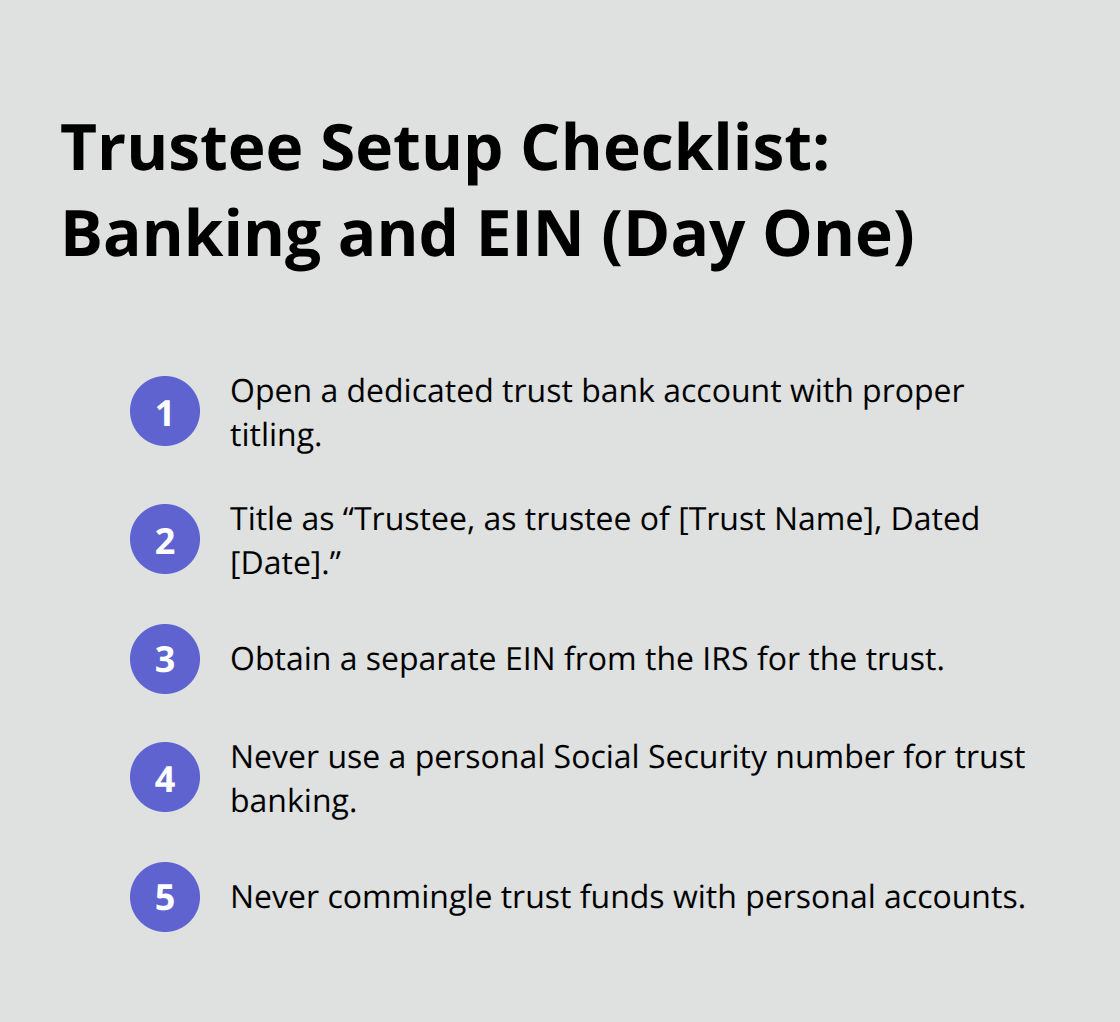

The trustee must then open a dedicated bank account titled as Trustee, as trustee of [Trust Name], Dated [Date], and obtain a separate tax identification number (EIN) from the IRS-never use personal Social Security numbers or combine trust funds with personal accounts. Failing to separate accounts invites disputes over what money belongs to whom and makes audits significantly harder.

Fiduciary Duty and Strict Adherence to Trust Terms

The trustee’s core fiduciary duty demands absolute loyalty to the trust’s terms and the beneficiaries’ best interests, which means following the exact language in the trust document, not personal preferences. If the trust says distributions happen when a beneficiary turns 30, the trustee cannot distribute earlier because a beneficiary asks. If the trust restricts distributions to health, education, maintenance, or support, the trustee must interpret those standards consistently and document each decision.

Trustees often face pressure from beneficiaries who disagree with restrictions, but bending the rules exposes the trustee to lawsuits from other beneficiaries and breach-of-fiduciary-duty claims. The trustee must also coordinate with professionals-a tax accountant, investment advisor, and attorney-because irrevocable trusts operate under complex rules that shift depending on whether the trust is a grantor trust (taxed to the grantor) or a non-grantor trust (taxed to the trust itself). This coordination prevents costly mistakes like missing tax filing deadlines or making distributions that trigger unexpected tax consequences.

Record-Keeping That Protects the Trustee and Beneficiaries

The trustee must maintain detailed records of every transaction: deposits, withdrawals, investment purchases and sales, distributions to beneficiaries, tax payments, insurance premiums, and professional fees. California law and fiduciary standards require this documentation to prove the trustee acted properly if disputes arise later. Many trustees underestimate how critical this is until a beneficiary questions where money went or an IRS agent asks for proof of compliance.

The trustee files Form 1041 annually for non-grantor trusts or provides a grantor letter for grantor trusts, detailing what income flows to the grantor versus the trust. Late or incorrect filings trigger penalties and audits that consume time and money.

Transparency and Communication With Beneficiaries

For beneficiaries, transparency reduces conflict more effectively than any other single action. Trustees should provide written accountings at least annually, showing beginning balances, income received, expenses paid, distributions made, and ending balances. Beneficiaries who understand the numbers trust the trustee; beneficiaries left in the dark assume mismanagement.

Some modern trustees use digital portals that give beneficiaries real-time access to account statements and distribution histories, which eliminates the excuse that information was unavailable. When distributing assets, the trustee must verify that each distribution complies with the trust’s terms, obtain signed receipts from beneficiaries, and keep copies in the trust file.

Special Considerations for Vulnerable Beneficiaries

If a beneficiary has special needs and receives government benefits like SSI or Medicaid, distributions must follow strict rules to avoid disqualifying the beneficiary-a mistake that can cost thousands in lost benefits. The trustee who takes time to get these mechanics right protects the trust’s assets, maintains beneficiary confidence, and avoids the litigation that destroys families and drains trust resources. Understanding these responsibilities sets the foundation for effective administration, but the trustee must also navigate the tax landscape that governs how irrevocable trusts operate and what obligations arise each year.

Tax Compliance and Fiduciary Reporting for Irrevocable Trusts

How Irrevocable Trusts Trigger Tax Obligations

Irrevocable trusts trigger tax obligations that revocable trusts avoid, and missing even one filing deadline costs money and invites IRS scrutiny. The IRS treats irrevocable trusts as separate taxpaying entities, which means the trustee must file Form 1041 annually if the trust earns income above $600, report distributions to beneficiaries on Schedule K-1, and track whether income flows to the trust or passes through to beneficiaries based on distribution status. State fiduciary income tax returns also apply in California and other states where the trust operates or holds property, adding another layer of compliance that many trustees overlook until penalties arrive.

Grantor Trusts Versus Non-Grantor Trusts

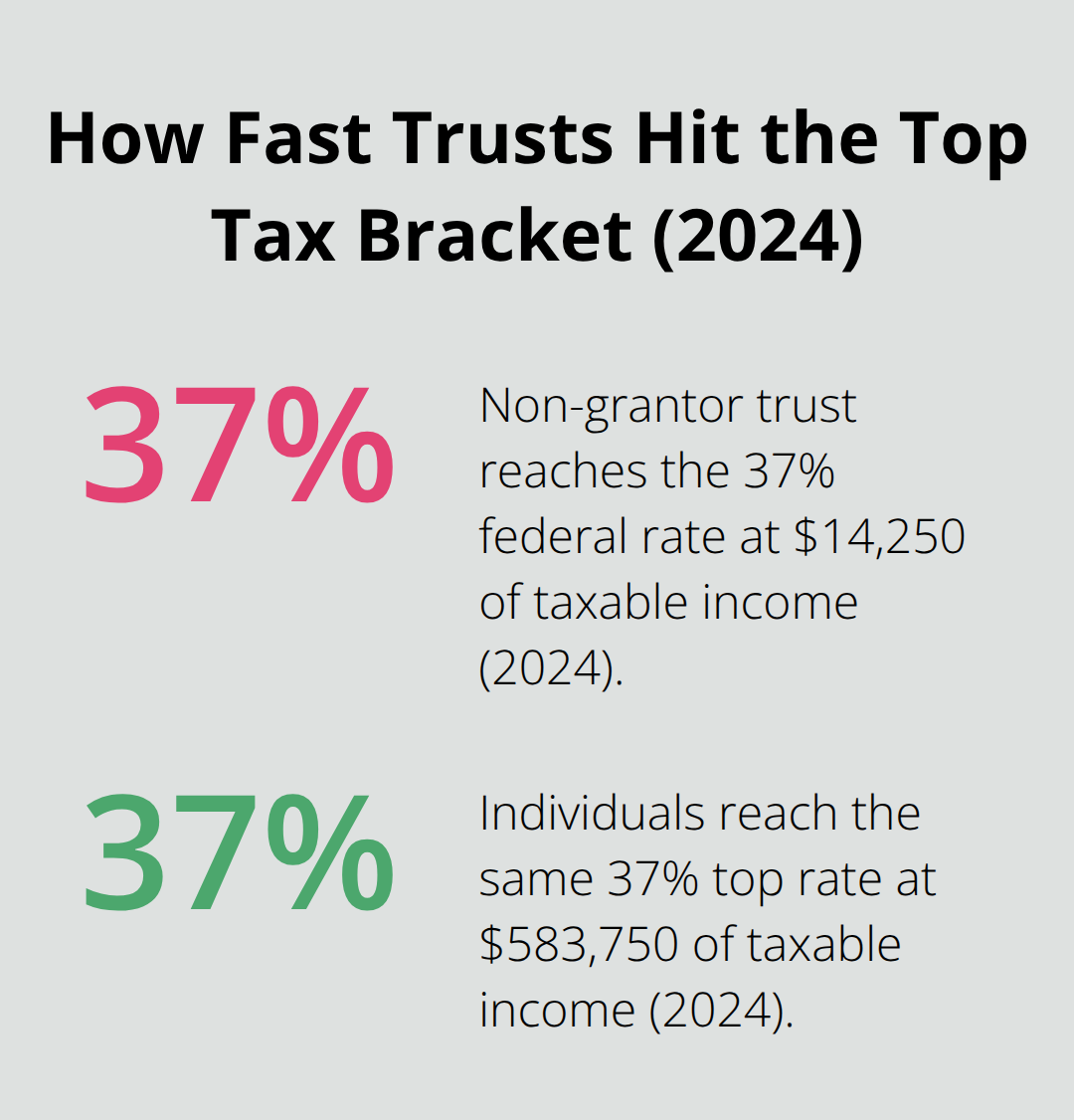

Grantor trusts-where the grantor retains certain powers-use the grantor’s Social Security number and the grantor pays income tax on all trust earnings, even if no distributions occur, which simplifies administration but concentrates tax liability on one person. Non-grantor trusts obtain their own EIN and file independently, splitting income between the trust and beneficiaries based on what each receives. The tax brackets for trusts compress dramatically: a non-grantor trust reaches the highest 37 percent federal rate at just $14,250 of taxable income in 2024, compared to $583,750 for individuals, meaning trustee decisions about distributions directly control how much tax the trust or beneficiaries owe. A trustee who accumulates income inside the trust instead of distributing it to beneficiaries forces the trust to pay punitive tax rates, while distributing income to beneficiaries in lower brackets saves thousands annually. This is not theoretical-it shapes whether a trust’s assets grow or shrink over time.

Estate Tax Planning and Asset Removal Strategies

Estate tax planning for irrevocable trusts centers on removing assets from your taxable estate before death, which directly reduces what the IRS can tax at death. The current federal estate tax exemption sits at $13.61 million per person in 2024, but Congress allowed this to sunset, dropping the exemption to approximately $7 million in 2026 unless legislation extends it-meaning couples who fail to act now could face unexpected estate tax liability in just two years.

Irrevocable life insurance trusts remove death benefits from taxable estates entirely; a $5 million policy outside a trust becomes part of your estate and triggers roughly $2 million in federal estate tax, while the same policy inside an ILIT passes tax-free to beneficiaries. Dynasty trusts use generation-skipping transfer tax exemptions to push wealth across multiple generations without depletion taxes at each level, though the grantor must file Form 709 when making taxable gifts to the trust to lock in exemption values.

Asset Protection Through Irrevocable Trust Structure

Asset protection within irrevocable trusts works because once assets transfer to the trust, creditors cannot reach them-the grantor no longer owns them-which shields against lawsuits, divorce claims, or business liability. This permanence is the trade-off: you cannot access the assets later without the trustee’s permission, but that restriction is precisely what makes the protection real. The structure itself creates the barrier that revocable trusts cannot provide. Proper structuring before funding occurs prevents costly mistakes that become expensive and often impossible to fix after the fact.

Final Thoughts

Irrevocable trust administration demands precision and ongoing attention because permanence leaves no room for correction. A missed filing deadline, miscommunicated distribution, or misinterpreted trust term triggers tax penalties, beneficiary disputes, or loss of asset protection that took years to build. The trustee who maintains detailed records, communicates transparently with beneficiaries, and coordinates with tax and legal professionals protects the trust’s assets and preserves family relationships far more effectively than one who treats administration as optional.

Professional guidance becomes essential when complexity exceeds your comfort level, particularly with life insurance trusts, dynasty planning, special needs beneficiaries, or multi-generational wealth transfer. The cost of professional help always proves less expensive than fixing administration errors after they occur, and the right planning today prevents costly problems tomorrow. We at Law Offices of Roshni T. Desai help clients establish irrevocable trusts correctly and navigate administration challenges with clarity and confidence across Southern California.

If you are establishing an irrevocable trust, administering one, or facing questions about whether an irrevocable structure fits your goals, contact us for a free consultation. Our team provides personalized guidance on trust structure, beneficiary communications, tax planning, and ongoing compliance to help you move forward with confidence.